- My Forums

- Tiger Rant

- LSU Recruiting

- SEC Rant

- Saints Talk

- Pelicans Talk

- More Sports Board

- Fantasy Sports

- Golf Board

- Soccer Board

- O-T Lounge

- Tech Board

- Home/Garden Board

- Outdoor Board

- Health/Fitness Board

- Movie/TV Board

- Book Board

- Music Board

- Political Talk

- Money Talk

- Fark Board

- Gaming Board

- Travel Board

- Food/Drink Board

- Ticket Exchange

- TD Help Board

Customize My Forums- View All Forums

- Show Left Links

- Topic Sort Options

- Trending Topics

- Recent Topics

- Active Topics

Started By

Message

re: Expiration of “Trump” tax cuts

Posted on 5/3/24 at 2:31 pm to SquatchDawg

Posted on 5/3/24 at 2:31 pm to SquatchDawg

quote:

So given this does it ever make sense to direct 100% of a company 401k into the tax deferred plan vs the Roth if it can drop you into the lower bracket?

Still makes sense. The brackets are adjusted for inflation every year so the standard deduction, the 15% threshold, etc will be higher when you're drawing from the 401k. Your expenses will be lower since your house is paid off. So you'll more likely than not be in a lower tax bracket.

1

1

Posted on 5/3/24 at 2:59 pm to Bestbank Tiger

Sorry…to be clear I was talking about a company sponsored tax deferred 401k vs a company sponsored after tax Roth 401k.

Are you saying the tax deferred is better?

I was under the assumption that the Roth was the way to go….so much so that people are actively converting traditional IRAs to Roths.

Are you saying the tax deferred is better?

I was under the assumption that the Roth was the way to go….so much so that people are actively converting traditional IRAs to Roths.

Posted on 5/3/24 at 3:03 pm to SquatchDawg

quote:

Sorry…to be clear I was talking about a company sponsored tax deferred 401k vs a company sponsored after tax Roth 401k.

Are you saying the tax deferred is better?

I was under the assumption that the Roth was the way to go….so much so that people are actively converting traditional IRAs to Roths.

I was saying pay the taxes later, since even with a higher rate in the future you're likely going to be in a higher bracket now.

Of course that's purely speculative. You could end up getting screwed if you use pretax dollars now.

Posted on 5/3/24 at 4:12 pm to SquatchDawg

quote:

was under the assumption that the Roth was the way to go….so much so that people are actively converting traditional IRAs to Roths.

I would imagine most people are converting Roths as a bridge from early retirement to 59.5. Or they are in a super low tax bracket. Or they fricked up and listened to Dave Ramsey who for some reason encourages everyone to do a back door Roth no matter what be their financial situation is.

It doesn't make a lot of sense (to me) to fund a Roth in your prime earning years when you're in a high bracket. Roths generally make the most sense when you're in a low tax bracket (i.e. early in your career).

Posted on 5/3/24 at 6:18 pm to SquatchDawg

quote:

Are you saying the tax deferred is better?

Often, yes. Many people mistakenly compare their top bracket today with their projected top bracket at withdrawal. As I tried to explain in earlier post, traditional withdrawals will usually be taxed at an effective rate lower that is lower because they will fill the lower brackets first (unless you have other income to fill those brackets in retirement.)

My guess is many people have mixed up the advice to fund a Roth IRA after maxing employer plans with the misguided advice that Roth 401k usually beats traditional 401k. Also, much advice is geared to new investors and thus skews to early career relatively lower earning years thus the advice to frontload Roth 401k. It's also a way of oversimplifying so new investors take action instead of getting stuck in analysis paralysis.

Posted on 5/3/24 at 7:05 pm to SquatchDawg

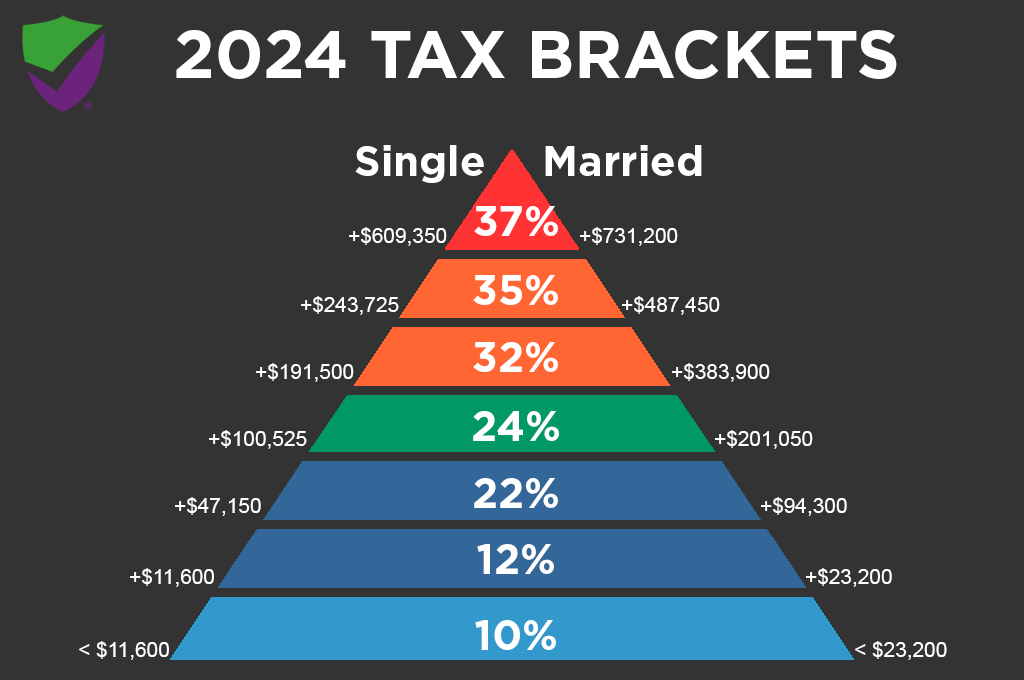

Example: married filing joint, $150k taxable income now, $150k annual retirement. Assumptions: no other retirement income, using 2024 brackets without inflation adjustment for simplicity sake (fair because not adjusting withdrawal amount for inflation either).

Tax bracket today: 22% thus each extra dollar you choose to pay tax on and contribute to Roth is taxed at 22% (thus only contributing .78¢) or you defer tax of 22% and contribute that full dollar to traditional.

At retirement the Roth balance will be 22% smaller than equivalent traditional contribution (unless you max annual contributions in which case to compare apples/apples you would invest the excess traditional tax savings either in a Roth IRA, taxable brokerage, etc)

Retirement Withdrawals from traditional are taxed at a lower EFFECTIVE RATE. First, $29k is tax free due to standard deduction. Next $23k taxed at 10% then additional up to $94k taxed at 12%. At that point you have ~$122k of withdrawals that have been taxed at rates from 0-12% (instead of 22% when you earned them) Only at that point does the last $18k get taxed in the 22% bracket.

Even if brackets are raised it isnt likely your bottom brackets will exceed the top rate you pay today (unles low income in which case Roth is easy choice.)

The math can still work in favor of traditional if you have other income in retirement but its a little more nuanced. You can have quite a bit of income before withdrawals are fully taxed in same bracket or higher than during contribution years. Of course there are other considerations such as triggering tax on SS benefits, ACA subsidy income limits, IRMAA, RMDs on traditional but not Roth etc. Thus, it is a good idea to have $ in multiple tax buckets so you can optimize where you pull from in retirement year to year based on needs and situation.

Tax bracket today: 22% thus each extra dollar you choose to pay tax on and contribute to Roth is taxed at 22% (thus only contributing .78¢) or you defer tax of 22% and contribute that full dollar to traditional.

At retirement the Roth balance will be 22% smaller than equivalent traditional contribution (unless you max annual contributions in which case to compare apples/apples you would invest the excess traditional tax savings either in a Roth IRA, taxable brokerage, etc)

Retirement Withdrawals from traditional are taxed at a lower EFFECTIVE RATE. First, $29k is tax free due to standard deduction. Next $23k taxed at 10% then additional up to $94k taxed at 12%. At that point you have ~$122k of withdrawals that have been taxed at rates from 0-12% (instead of 22% when you earned them) Only at that point does the last $18k get taxed in the 22% bracket.

Even if brackets are raised it isnt likely your bottom brackets will exceed the top rate you pay today (unles low income in which case Roth is easy choice.)

The math can still work in favor of traditional if you have other income in retirement but its a little more nuanced. You can have quite a bit of income before withdrawals are fully taxed in same bracket or higher than during contribution years. Of course there are other considerations such as triggering tax on SS benefits, ACA subsidy income limits, IRMAA, RMDs on traditional but not Roth etc. Thus, it is a good idea to have $ in multiple tax buckets so you can optimize where you pull from in retirement year to year based on needs and situation.

This post was edited on 5/3/24 at 7:08 pm

Posted on 5/3/24 at 7:21 pm to FinleyStreet

quote:

He should've made the individual rate cuts permanent and the corp rates temporary instead of the other way around.

I think the thought was it’s going to be difficult to get corp rate cuts to pass again and easier to pressure Dems into passing something for individuals.

This thread is an example. If the corp rate cuts were the ones sunsetting right now, we wouldn’t even be talking about it.

Posted on 5/3/24 at 7:21 pm to TorchtheFlyingTiger

That’s definitely something to ponder.

Most material I’ve seen pushes 100% Roth due to the assumption that taxes will be much higher in the future. Especially in 10 years (my window) when SS and Medicare will be at th breaking point. Even though the plan is to have everything paid off so I expect expenses to be much lower at retirement.

That said, the majority of my retirement savings is still in traditional from my younger years when a Roth wasn’t an option but if these rates change I may consider switching over to get out of the higher bracket for that full contribution amount.

Thanks!

ETA..also, we’ve had a pretty low effective tax rate for years with two kids and a rental. But the rental is almost fully depreciated and with these changes if they happen that could make sense.

Most material I’ve seen pushes 100% Roth due to the assumption that taxes will be much higher in the future. Especially in 10 years (my window) when SS and Medicare will be at th breaking point. Even though the plan is to have everything paid off so I expect expenses to be much lower at retirement.

That said, the majority of my retirement savings is still in traditional from my younger years when a Roth wasn’t an option but if these rates change I may consider switching over to get out of the higher bracket for that full contribution amount.

Thanks!

ETA..also, we’ve had a pretty low effective tax rate for years with two kids and a rental. But the rental is almost fully depreciated and with these changes if they happen that could make sense.

This post was edited on 5/3/24 at 7:25 pm

Posted on 5/3/24 at 11:08 pm to SquatchDawg

I retired early 5 years ago and am still under SS eligibility age. We have no income except for passive (interest and investment) income. For the past 3 tax years I've been aggressively rolling over Traditional IRA to Roth staying under the tax bracket I wanted to stay under. This makes the 4th and final year for the rollovers. Now all my retirement account investments are about 85% Roth with the rest split between HSA and traditional IRA. I knew I wanted to take advantage of lower taxes before 2025. My gut was telling me that taxes even though high are at a discount compared to what I suspect will happen in 2025 and later.

I also never wanted to get to 100% Roth. I wanted to maintain Traditional IRA amounts to take advantage of the annual standard deductions. Plus it makes it much easier to pay annual income taxes via a single Fidelity Traditional IRA withdrawal in December each year than it is to estimate and pay quarterly income taxes. Fidelity withholds and pays our Federal and State income taxes as I specify at the end of each year with a single withdrawal.

I also never wanted to get to 100% Roth. I wanted to maintain Traditional IRA amounts to take advantage of the annual standard deductions. Plus it makes it much easier to pay annual income taxes via a single Fidelity Traditional IRA withdrawal in December each year than it is to estimate and pay quarterly income taxes. Fidelity withholds and pays our Federal and State income taxes as I specify at the end of each year with a single withdrawal.

Posted on 5/3/24 at 11:19 pm to slackster

quote:

SALT cap would be removed

This is why Democrats would probably not support it. SALT deductions are big in high tax states, so for their voter interests it's their calculation that letting taxes go up by letting those sunset, BUT also getting the SALT back is a net win for them.

This post was edited on 5/3/24 at 11:19 pm

Posted on 5/4/24 at 7:00 am to Teddy Ruxpin

Biden’s press secretary said they’re going to magically only sunset for people making over 400k.

“But the law doesn’t work that way. It’s going to sunset for everybody not just those making over 400k…”

“The President has made it very clear he’s not going to raise taxes on anybody making over 400k”

Thanks so much for the clarity…

Thanks so much for the clarity…

“But the law doesn’t work that way. It’s going to sunset for everybody not just those making over 400k…”

“The President has made it very clear he’s not going to raise taxes on anybody making over 400k”

Posted on 5/4/24 at 7:28 am to TorchtheFlyingTiger

quote:

TorchtheFlyingTiger

Multiple bucket strategy provides a great hedge on the unknown. Definitely preferred approach.

Posted on 5/4/24 at 10:47 am to lynxcat

Multiple bucket is great but most people learn about it later in life when traditional 401k probably makes the most sense at their marginal income rates.

In your 20s and maybe even your 30s you should be making Roth IRAs and putting anywhere from the company match % to the annual maximums in Roth 401ks if available. Provides alot of flexibility early and typically at lower marginal rates. Traditional 401k from the 22% bracket onward and/or later in life.

In your 20s and maybe even your 30s you should be making Roth IRAs and putting anywhere from the company match % to the annual maximums in Roth 401ks if available. Provides alot of flexibility early and typically at lower marginal rates. Traditional 401k from the 22% bracket onward and/or later in life.

Posted on 5/5/24 at 8:32 am to slackster

Jumping on this thread. Would it really be a net bad?

Personal exemptions come back. Assuming they would be adjusted so 5000 per. My itemized deductions are right at 28000. Plus salt cap goes away so that would be and extra 18k or so. That’s 38k in extra deductions. My guess is it would almost be a wash.

Personal exemptions come back. Assuming they would be adjusted so 5000 per. My itemized deductions are right at 28000. Plus salt cap goes away so that would be and extra 18k or so. That’s 38k in extra deductions. My guess is it would almost be a wash.

Posted on 5/5/24 at 9:19 am to Fat Bastard

quote:

they love raising taxes.

Someone has to pay for all the illegals do do pants is letting in the country

most with nothing

Posted on 5/6/24 at 1:45 pm to The Torch

The problems are much bigger than this. How many years have we spent way more money than we bring in? Both Democrat and Republican focus on re-election vs running the country like a business and have for the majority of our existence. We have only had 3 or 4 balanced budgets in the past 50 years or so. Something has to be done with the looming social security shortage. Blaming it on illegals sounds good to some, but this is a much bigger problem than that!

Posted on 5/7/24 at 12:46 pm to SquatchDawg

Don't forget: the Obamacare Cliff also returns at the same time....

For a lot of people, that will be bigger than the sunset of the Trump Tax Cuts, though I think your $200K family example may not get burned, a 150 K family who needs Obamacare may feel a big bite.

For a lot of people, that will be bigger than the sunset of the Trump Tax Cuts, though I think your $200K family example may not get burned, a 150 K family who needs Obamacare may feel a big bite.

Posted on 5/7/24 at 3:07 pm to SquatchDawg

quote:

So my follow up question is where are our esteemed Republican congressmen pushing a bill to make this permanent?

God I hate politicians.

They were too busy trying to keep trump from being president.

Posted on 5/7/24 at 4:40 pm to Teddy Ruxpin

quote:

This is why Democrats would probably not support it. SALT deductions are big in high tax states, so for their voter interests it's their calculation that letting taxes go up by letting those sunset, BUT also getting the SALT back is a net win for them.

Republicans should be pushing for SALT to be 100% non deductible and call the deduction what it is, a massive tax break for the 1%.

Posted on 5/7/24 at 8:12 pm to BlackAdam

quote:

Republicans should be pushing for SALT to be 100% non deductible and call the deduction what it is, a massive tax break for the 1%.

Yep. It’s a cap that mainly affects the rich and it’s a subsidy for states that have higher taxes.

Of course a lot of states have already started the workaround on this limitation

Page 2 of 3

Page 2 of 3

Popular

Back to top